When the housing crisis and economic recession hit, it put many prospective home buyers’ plans on hold, forcing those considering purchasing a home into the rental market. Now, as the economy continues to improve, some of those renters are looking to own.

However, there are many factors to consider when buying a home. When it comes to the closing process, it is a good idea to know the terminology that will be discussed. This can help make the situation much more comfortable and professional for all parties involved. Below are some of the terms that may be discussed during the closing process.

5 Mortgage Closing Terms Every Buyer Should Know

ANNUAL PERCENTAGE RATE (APR) This term reflects the cost of all credit and finances as determined by the length of a year, including the interest rate, points, broker fees, and other credit charges obligated to the buyer.

PRIVATE MORTGAGE INSURANCE (PMI) PMI is typically required if a borrower puts a down payment that’s less than 20% of the home’s value.

The charge is usually included in the monthly mortgage payment in an attempt to protect the lender from possible default.

DOWN PAYMENT Like many transactions involving large sums of money, the mortgage process involves a down payment – the amount a home buyer pays in order to make up the difference between the purchase price and the mortgage amount. Some experts advise no less than 10% to 15%. However, any amount over 20% of the purchase price is often recommended, and may be required to avoid having to pay for private mortgage insurance.

LOAN ESTIMATE (LE) The Consumer Financial Protection Bureau, or CFPB, requires your lender to issue a Loan Estimate within three business days of receiving your mortgage application. The Loan Estimate details the terms of your loans along with estimated closing costs.

CLOSING COSTS Closing costs may also be referred to as transaction costs or settlement costs and may include various fees and charges associated with finalization. These may include or be related to application fees, title examination, title insurance, property fees, as well as settlement documents and attorney charges.

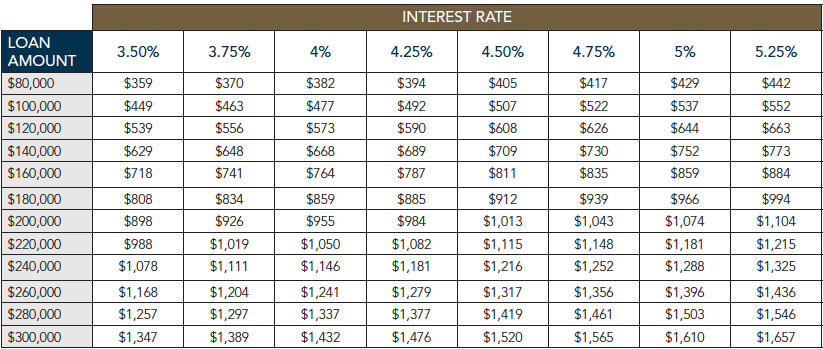

Sample Mortgage Payment

30-YEAR LOAN / PRINCIPAL & INTEREST ONLY

THIS FORMULA IS ONLY A GUIDE AND NOT TO BE CONSTRUED AS ACTUAL LENDING CALCULATIONS.

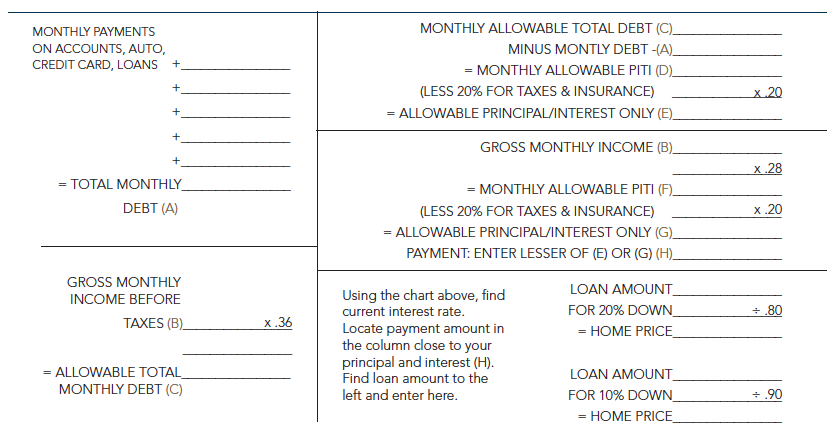

How Much Home Can You Afford?

Contact your loan officer to determine more accurately what price range you should consider. Lenders abide by certain ratios when calculating the loan amount their customers can qualify for and the ratios vary by lender and loan program. Many use 28% of your gross monthly income as the maximum allowed for your mortgage payment (principal/interest/taxes/ insurance or PITI); for your total monthly debt, the ratio is 36%. Total monthly expenses means PITI plus long-term debt (such as auto loans) and revolving/credit-card debt. Do not include other expenses such as groceries, utilities, clothing, tuition, etc., to calculate this ratio.

The Ultimate First-Time Home Buyer Guide